Recently I posted an article on a subject that is near and dear to mobile operators, customer acquisition and retention. It related to the publication by Next Generation Community host Nokia (News - Alert) of its 10th in a series of reports titled appropriately, Nokia 2016 Acquisition and Retention Study. It was noted that there were several categories that make the report a very useful resource. In fact, this week Nokia has published the details on the part of the series of this report dealing with “Drivers of Customer Retention.” And once, again, there is a lot to evaluate in the findings.

As Nokia research found, there are four major drivers of customer retention:

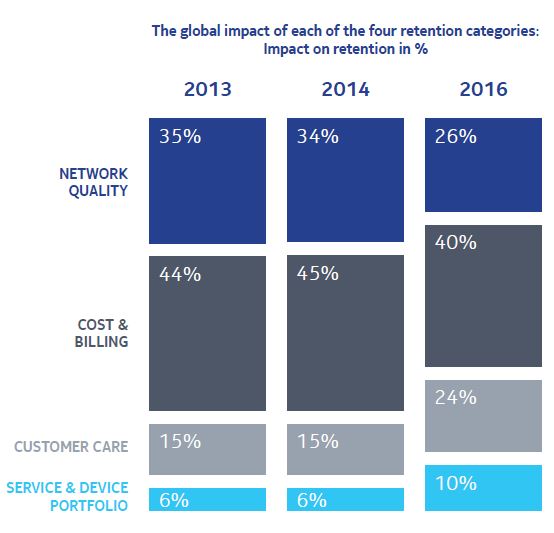

Source (News - Alert): Nokia 2016 Acquisition and Retention, Drivers of Customer Retention

Source (News - Alert): Nokia 2016 Acquisition and Retention, Drivers of Customer Retention

As mentioned in the previous article, what is clearly noteworthy in looking at the year-over-year comparisons is that while cost and billing remain the dominant concerns of mobile service customers in determining which provider they would like to use, the rapid ascent of customer care along with the service and device portfolio should be considered as calls for action. What is surprising as the decline of network quality as a driver which is likely attributable to quality being perceived as being related somewhat to network coverage as well and thanks to competition in virtually every market globally differentiation between services on this score is likely to be perceived as being almost a level playing field.

That said, customer care is worth a shout out here. As the report explains, customer care as a category is comprised of three aspects:

- Self Care

- Request & Complaint Handling

- General Customer Service

Each holds varying degrees of significance across the “mature” and “transition” markets described in the report, but as can be seen from the graphic, globally Request & Complaint Handling and General Customer Service, play the most significant roles in driving the overall importance.

In speaking with Josh Aroner, Vice President, Applications & Analytics Marketing, Nokia about the series in general and about customer care, he explained that: “Customers want greater transparency in billing and bundling, they want their problems handled by skilled professionals quickly and satisfactorily, and they want their services to be personalized and their care customized to meet their needs.”

He added that service providers should understand from the research that, “The experience is everything and service providers have unique opportunities to leverage providing great experiences.” He noted that this relates to all aspects of the customer experience and not just when they are interacting based on the need to resolve a problem.

Aroner also observed that one of the reasons service providers are uniquely positioned to attract and retain customers, even in a world where there is now OTT competition along with competition from traditional providers, is that companies have usage data and other information directly related to the entire customer journey. This information when properly shared and analyzed can enable service providers to create and sustain differentiated value.

I added, and Aroner agreed, that the emergence of concerns over security is also a nice way for service providers to create what used to be called, “stickiness.”

Next up in the series will be, “Trends in New Sign-ups.”

Edited by Maurice Nagle

Internet Telephony Magazine

Click here to read latest issue

Internet Telephony Magazine

Click here to read latest issue CUSTOMER

CUSTOMER  Cloud Computing Magazine

Click here to read latest issue

Cloud Computing Magazine

Click here to read latest issue IoT EVOLUTION MAGAZINE

IoT EVOLUTION MAGAZINE